TL;DR

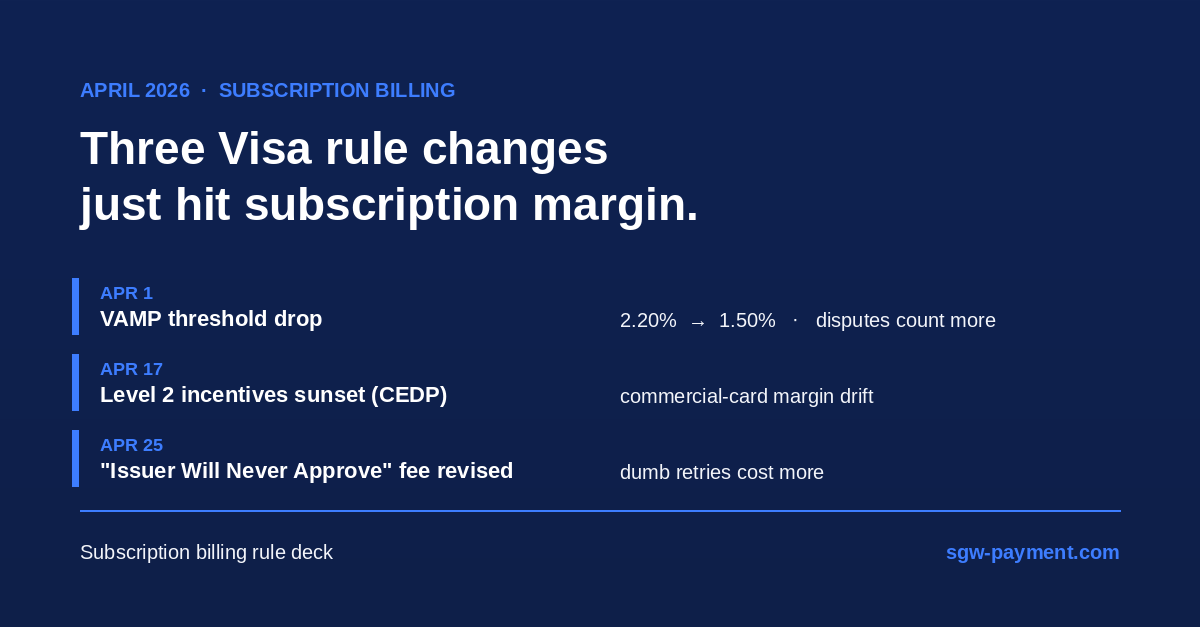

- Visa rolled out three subscription-billing-relevant rule changes between April 1 and April 25, 2026: the VAMP "Excessive" dispute threshold dropped from 2.20% to 1.50%, Level 2 commercial-card interchange incentives sunset under CEDP, and the international "Issuer Will Never Approve" reattempt fee was revised.

- The compound effect for subscription companies: dumb retries cost more, disputes count more, and B2B commercial-card cohorts drift to higher-cost tiers without enriched data.

- The durable answer is cascading PSP routing across multiple acquirers, decline-code-aware retry logic, and a multi-MID volume strategy — not a denser dunning loop.

What changed in April 2026

Three Visa rule changes affecting subscription billing took effect within a 25-day window.

April 1 — VAMP threshold drop. The Visa Acquirer Monitoring Program’s "Excessive" threshold for merchant chargeback ratios dropped from 220 basis points (2.20%) to 150 basis points (1.50%) across the US, EU, Canada, and Asia-Pacific. The VAMP ratio is calculated as (Fraud TC40 + Disputes TC15) / Settled TC05 — a volume-based count, not a dollar-weighted one. Merchants under 1,500 combined fraud + dispute events per month are not enrolled, but anyone above that floor is now operating with a tighter ceiling. Acquirers face stricter portfolio-level thresholds, which will translate to downstream pressure on individual merchant accounts.

April 17 — Level 2 commercial-card incentives sunset under CEDP. Visa retired the legacy Level 2 interchange incentive program for Visa Business, Corporate, and Purchasing credit transactions, transitioning to the Commercial Enhanced Data Program (CEDP). Under CEDP, eligible transactions that pass the required commercial data fields stay in the favorable rate band; transactions that don’t pass enriched data drop to standard interchange tiers. For B2B SaaS merchants relying on commercial-card cohorts, this is a quiet basis-point hit unless billing systems are passing the right Level 2/3 data to the acquirer.

April 25 — "Issuer Will Never Approve" reattempt fee revised. Visa revised the international rate on the System Integrity International Fee (the "Issuer Will Never Approve" reattempt fee). The fee itself isn’t new — it has been live since April 2022 at $0.10 domestic and $0.15 international per attempt — but the international rate has now moved. The trigger remains unchanged: any retry on a Category 1 decline (issuer responses indicating the card is blocked, lost, stolen, closed, or never existed) is treated as non-compliant and assessed the fee on every reattempt. The fee appears on merchant statements as VI NEVER APPROVE REATTEMPT FEE.

Why this matters for subscription billing

Subscription companies are structurally over-exposed to all three changes — and the exposures compound.

Dunning loops generate Category 1 retry waste. A typical involuntary churn flow re-presents a failed payment two or three times over a 7–14 day window. When the first decline is a Category 1 response, the issuer is telling Visa the card will never approve. Naïve dunning logic that retries on a fixed cadence regardless of decline-code category bills the Never-Approve fee on every retry, on every cohort, every month — a margin leak that runs on autopilot until someone instruments the statement line.

VAMP math punishes volume-driven dispute generation. The new 1.50% threshold is volume-based, which means subscription cohorts with high transaction frequency and meaningful dispute density (refunds, free-trial-to-paid conversions, "I forgot I subscribed" chargebacks) will drift toward the threshold faster than acquirers expected. Once a merchant crosses Excessive, enforcement fees apply and acquirers face downstream portfolio pressure that flows back as account reviews and tightened terms.

CEDP changes reshape B2B SaaS margins quietly. Commercial-card transactions that used to fall under Level 2 incentives need to pass enriched data to stay in the favorable band. Subscription billing systems built five or six years ago often pass minimal data — the fields work, the transactions clear, and nobody notices the basis-point drift on the commercial-card share until a year of statements is reconciled.

The single thread connecting all three: subscription billing infrastructure built on assumptions from the 2018–2022 rule set is misaligned with the April 2026 rule set, and the misalignment shows up first as fee creep, not as broken transactions.

How payment orchestration absorbs the shift

The mechanism that absorbs all three changes at once is orchestration — specifically, three concrete capabilities.

Decline-code-aware retry. Smart retry logic that respects Visa’s Category 1 / Category 2 / Category 3 taxonomy treats a Category 1 decline as terminal for the original card and either skips the retry entirely or pivots to a card-update path (account updater, customer-driven re-collection). Retries are reserved for Category 2 and 3 codes where the issuer might approve a later attempt under different conditions. The Never-Approve fee stops appearing on the statement.

Cascading PSP routing across acquirers. When a soft decline hits one acquirer’s path, the next attempt routes through a different acquirer with a different scheme path — not a retry on the same PSP. Cascading reduces same-card-same-acquirer retry pressure (the Visa Excessive Reattempts rule lives in this neighborhood too) and gives subscription billing access to multiple acquirer relationships without the integration cost of running multiple gateways in parallel.

Multi-MID volume distribution. VAMP’s volume-based math means a merchant operating one MID with 100% of its dispute volume sees a different ratio than a merchant operating three MIDs across geographies and card brands. Multi-MID strategy — a structural piece of the orchestration layer — distributes risk across MIDs and acquirer portfolios so a single bad cohort doesn’t push the whole book over the threshold.

None of this is theoretical. The April 2026 rule deck is live now; the first merchant statements reflecting the new fees will land in June. The interval between today and June is the window to instrument billing logic against the new rule set.

Takeaways

- Pull a 90-day sample of failed-payment retries and tag them by Visa decline-code category. Any retry on a Category 1 code is a Never-Approve fee waiting to bill.

- Recalculate the VAMP ratio on rolling 30-day windows per MID and per acquirer. The headline number is volume-based, but the ceiling is now 1.50% — not the 2.20% your last quarterly review assumed.

- Audit commercial-card transaction data for Level 2/3 field completeness. Anything not passing enriched data is drifting to standard interchange under CEDP.

- Push retry logic upstream of the PSP — decline-code-aware retry plus cascading routing across acquirers absorbs all three changes in a single mechanism.

- Treat the gap between today and the June statement cycle as a fee-instrumentation window, not a quiet quarter.

Sources

- Visa Core Rules and Visa Product and Service Rules — 18 April 2026

- April 2026 Interchange and Network Fee Updates — Wind River Payments

- VAMP 2026: What Changes on April 1 — Basis Theory

- The Visa Acquirer Monitoring Program (VAMP) — Equifax

- Visa Issuer Never Approve Fee — Merchant Cost Consulting

- Visa CEDP 2025 Credit Card Rules Changes — Priority Commerce

- Crucial Update: Visa’s Level 2 Interchange is Sunsetting — Beacon Payments

About SGW Payment — SGW Payment is a payment orchestration platform built for global digital subscription businesses. With one API, SGW connects merchants to a network of PSPs and acquirers, intelligently routes every transaction for the best success rate and lowest cost, and reconciles fees end-to-end — so payments stop being a constraint and start being a growth lever. Learn more at sgw-payment.com.