TL;DR

- Three M&A waves crashed through the merchant payments stack over the last 12 months: Global Payments closed its $24.25B acquisition of Worldpay on January 12, 2026; the orchestration vendor base consolidated (Worldline/PaymentIQ €160M, PayRetailers/Celeris, TokenEx/IXOPAY); and Global Payments separately swallowed takepayments in the UK.

- The post-Worldpay Global Payments now sits across 6 million merchant locations, $3.7 trillion in volume, and 175 countries. Counterparty concentration just rose at every layer of the merchant payments stack.

- For subscription companies, single-PSP architecture is no longer a sourcing decision — it’s a bet on the M&A activity of one private-sector counterparty. Orchestration absorbs the bet.

The 12 months of consolidation

The single most consequential merchant-payments deal of the cycle closed on January 12, 2026: Global Payments completed its $24.25 billion acquisition of Worldpay from FIS and GTCR. Same day, FIS bought Global Payments’ Issuer Solutions business (the former TSYS) for $13.5 billion. The combined Global Payments now spans 6 million merchant locations, $3.7 trillion in annual processing volume, and 175 countries.

That deal sits inside a wider consolidation pattern that has reshaped the orchestration vendor base in parallel:

- Worldline → Incore Invest (PaymentIQ, €160M, closed March 2, 2026). Worldline divested its payments orchestration platform to a Stockholm-based investor as part of its “North Star” refocus on core European payment activities. PaymentIQ now operates as a standalone company.

- PayRetailers → Celeris (June 26, 2025). The Spanish processor acquired the Amsterdam-based orchestration platform that connected merchants to 75+ acquiring partners through a single API.

- TokenEx + IXOPAY (closed February 2025). Tokenization and orchestration combined under the IXOPAY brand.

- Global Payments → takepayments (June 2024, ~$250M). Earlier in the same cycle, Global Payments bought the UK acquirer serving 75,000 merchants — a UK-specific tightening that previewed the larger Worldpay deal 18 months later.

The market data tells a consistent story. The payment orchestration platform market is sized at $2.65 billion in 2025 and projected at $7.27 billion by 2031 — an 18.31% CAGR. Categories that grow that fast consolidate that fast.

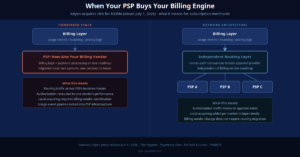

What changes for a subscription business when a PSP is acquired

Acquisitions are priced for the acquirer’s strategy, not the merchant’s billing stability. The operational drag the deal didn’t price in lands on the merchant’s desk in the form of:

- Contract reviews. Standard MFN, exclusivity, pricing-floor, and termination clauses get revisited. Anything that the acquired entity could once negotiate flexibly may now sit behind a larger group’s commercial policy.

- Integration migrations. APIs deprecate, endpoints rename, certificates rotate on the acquirer’s calendar. Merchants who built tightly to a single PSP’s idiosyncrasies are the ones who absorb the migration cost.

- Support-quality regression. Account managers reshuffle, SLAs are restated against the parent’s standards, escalation paths lengthen — this typically lasts 6–12 months post-close.

- Regional-coverage shifts. Acquirers cherry-pick the geographies they keep prioritizing. Smaller markets that the acquired company was actively serving may slip down the roadmap.

- MID continuity questions. When two acquirer portfolios merge, MID strategies (limits, currencies, vertical mix) get reassessed. A high-risk subscription cohort that fit comfortably under the acquired entity’s risk appetite may not fit the parent’s.

For a subscription business, none of this is catastrophic on day one. It is an accumulation of small frictions that compress conversion, cost margin basis points, and consume engineering time that should have gone to the product.

Why the orchestration M&A is its own signal

A natural reaction to acquirer concentration is “switch to an orchestration vendor and let them solve it.” The 2024–2026 pattern complicates that. The orchestration *vendors themselves* are consolidating — being acquired by processors (Celeris by PayRetailers), bought by investors (PaymentIQ by Incore Invest), or merged with adjacent infrastructure (TokenEx with IXOPAY).

What this means: the value the merchant is buying isn’t a *vendor*; it’s an *architecture*. A multi-PSP, one-API, cascading-fallback architecture survives orchestration vendor M&A because it isn’t bound to any single relationship. A single-vendor “orchestration” deployment that outsources all the routing to one partner inherits the same vendor-concentration risk it was supposed to fix.

How payment orchestration absorbs the shift

The structural hedge against acquirer and orchestration consolidation has three concrete capabilities:

One API, multiple acquirers. A merchant integrates once. Behind that integration sit multiple PSPs and acquiring relationships. When any single counterparty is in transition, transactions keep flowing through the others without an API change on the merchant side.

Cascading PSP routing with transactional fallback. A soft decline at acquirer A automatically retries at acquirer B with a different scheme path, not at acquirer A on the same MID. Merchants stop being held hostage by a single PSP’s approval rates, fee schedule, or technical incidents.

Multi-MID portfolio strategy. MIDs are spread across acquirer portfolios, geographies, and currencies — not concentrated under a single counterparty. When one parent group reassesses risk appetite or adjusts policy, the merchant’s volume continues to clear elsewhere.

These are the same capabilities that absorb fee creep and scheme-rule changes; they also happen to be the ones that absorb counterparty concentration. The mechanism is the same: don’t be dependent on any single PSP.

Takeaways

- Pull a list of every PSP, acquirer, and gateway your billing stack touches. Mark the ones that have changed parent ownership in the last 12 months. Anything on that list is in transition risk.

- For each vendor flagged, identify the contract clause that lets the merchant exit cleanly: termination notice, data-portability, MID-portability. Test that the playbook works *before* a renegotiation lands.

- Audit the “single point of failure” tier of the stack. If 100% of recurring billing volume routes through one PSP, the merchant’s margin is exposed to that PSP’s M&A calendar, not its product roadmap.

- Treat orchestration as an architecture, not a vendor. The architecture (multi-PSP, one API, cascading fallback) is what survives the next round of consolidation.

- Re-cut the MID strategy by acquirer concentration, not by geography. Geographic diversification is real; counterparty diversification is the layer most teams miss.

Sources

- Global Payments completes $24.25bn Worldpay deal — Payment Expert (12 Jan 2026)

- Global Payments closes Worldpay purchase, issuer sale to FIS — American Banker

- FIS Completes Strategic Acquisition of Global Payments’ Issuer Solutions Business — BusinessWire (12 Jan 2026)

- Worldline announces the finalisation of the divestment of PaymentIQ — Worldline (2 Mar 2026)

- Worldline sells CoreOrchestration to Incore Invest for €160m — FintechFutures

- PayRetailers acquires payment orchestration fintech Celeris — FintechFutures

- Global Payments acquires UK’s takepayments — FintechFutures

- TokenEx and IXOPAY Merge — IXOPAY

- Payment Orchestration Platform Market Report — Mordor Intelligence

About SGW Payment — SGW Payment is a payment orchestration platform built for global digital subscription businesses. With one API, SGW connects merchants to a network of PSPs and acquirers, intelligently routes every transaction for the best success rate and lowest cost, and reconciles fees end-to-end — so payments stop being a constraint and start being a growth lever. Learn more at sgw-payment.com.